New York Washington, D.C. Los Angeles Palo Alto London Paris Frankfurt Brussels

Tokyo Hong Kong Beijing Melbourne Sydney

www.sullcrom.com

August 1, 2023

Basel III ‘Endgame’

Regulators Propose Significant Revisions to Capital Rules Applicable

to Large Banks

SUMMARY

On July 27, 2023, the Federal Reserve, the FDIC, and the OCC issued a proposal that would result in

significant changes to the U.S. regulatory capital rules for banking organizations with total consolidated

assets of $100 billion or more.

1

As previewed by Federal Reserve Vice Chair for Supervision Barr,

2

the agencies estimate that the

proposal would increase risk-weighted assets (“RWAs”) (i.e., the denominator of risk-based capital ratios)

by 20 percent in the aggregate across affected banking organizations at the holding company level,

although the agencies note that the estimated effects vary meaningfully across those organizations.

3

The interagency proposal, often referred to as “Basel III Endgame,” would implement both (i) the

standards that the Basel Committee on Banking Supervision published in December 2017 to finalize the

post-crisis Basel III reforms

4

and (ii) the Basel Committee’s revised standard for market risk capital

requirements finalized in February 2019, referred to as the “Fundamental Review of the Trading Book” or

“FRTB.”

5

The proposal also would make other targeted revisions to the U.S. capital rules.

Also on July 27, the Federal Reserve proposed to revise the surcharge applicable to U.S. global

systematically important banks (“GSIBs”).

6

The Federal Reserve approved the Endgame proposal by a vote of 4-to-2, with Governors Bowman and

Waller dissenting, and approved the GSIB surcharge proposal by a vote of 6-to-0. The FDIC approved

the Endgame proposal by a vote of 3-to-2, with Vice Chairman Hill and Director McKernan dissenting.

The Endgame and GSIB surcharge proposals reflect two elements of the “holistic review” of bank capital

requirements undertaken by Vice Chair for Supervision Barr.

7

In addition to these proposals, Vice Chair

-2-

Basel III ‘Endgame’

August 1, 2023

Barr has indicated that there will be additional proposals relating to regulatory capital and related matters,

including a potential extension of long-term debt requirements to banking organizations with assets of

$100 billion or more and revisions to the standardized liquidity requirements applicable to large banking

organizations.

8

Comments on both proposals are due November 30, 2023.

9

We expect the proposals will be subject to

extensive comment by affected banking organizations and other market participants.

OVERVIEW AND OBSERVATIONS

A. Endgame Proposal

In general, consistent with the Basel Committee’s December 2017 and FRTB publications, the Endgame

proposal focuses primarily on the calculation of RWAs. Certain aspects of the proposal would, however,

also affect the components of regulatory capital (i.e., the numerator of risk-based and leverage capital

ratios). Notably, subject to a phase-in period, Category III and Category IV banking organizations (i.e.,

non-GSIB banking organizations with $100 billion to $700 billion in total consolidated assets and less than

$75 billion in cross-jurisdictional activity) would no longer be permitted to opt out of including certain

components of accumulated other comprehensive income (“AOCI”) in regulatory capital. As a result,

unrealized gains and losses on available-for-sale (“AFS”) debt securities would flow through regulatory

capital ratios for these banking organizations.

10

The agencies estimate that the proposed revisions “would have the effect of modestly increasing capital

requirements for lending activity,”

11

but argue that, “[a]lthough a slight reduction in bank lending could

result from the increase in capital requirements, the economic cost of this reduction would be more than

offset by the expected economic benefits associated with the increased resiliency of the financial

system.”

12

A number of statements released in connection with the proposal addressed cost-benefit considerations.

Federal Reserve Chair Powell, for example, noted that “[w]hile there could be benefits of still higher

capital, as always we must also consider the potential costs,” adding that “[t]his is a difficult balance to

strike, and striking it will require public input and thoughtful deliberation.”

13

Chair Powell also observed

that, although “[h]igh levels of capital are essential to enable banks to continue to lend to households and

businesses and conduct financial intermediation, even in times of severe stress,” “raising capital

requirements also increases the cost of, and reduces access to, credit.”

14

Federal Reserve Governor

Jefferson also expressed “concern” regarding the potential effects of the proposal on “lend[ing] to

businesses and individuals.”

15

For trading activities, the agencies estimate that capital requirements would “increase substantially,

though the specific outcome will depend on banking organizations’ implementation of internal models.”

16

More specifically, the Federal Reserve staff memorandum accompanying the proposal estimates that

-3-

Basel III ‘Endgame’

August 1, 2023

capital requirements for trading activities would “more than doubl[e] for some firms.”

17

The extent of the

proposed increase in capital requirements for trading activities was another area of focus in a number of

statements accompanying the proposal. Chair Powell, for example, cautioned that “the proposed very

large increase in risk-weighted assets for market risk overall requires us to assess the risk that large U.S.

banks could reduce their activities in this area, threatening a decline in liquidity in critical markets and a

movement of some of these activities into the shadow banking sector.”

18

Based on year-end 2021 data, the agencies estimate that some large banking organizations would face a

capital shortfall if the proposal were finalized in its current form.

19

However, Vice Chair Barr has

suggested that, for banking organizations that would need to build capital to satisfy the new requirements,

the increased capital requirements could be satisfied “through retained earnings in less than two years,

even while maintaining their current dividends.”

20

Although not expressly stated, this two-year timeline

appears predicated on the suspension of share repurchases. In addition, it is unclear whether this two-

year timeline takes into account the fact that, in the ordinary course, banking organizations operate with

capital levels in excess of applicable requirements.

The agencies characterize the proposed Endgame revisions as “generally consistent with recent changes

to international capital standards issued by the Basel Committee.”

21

A number of statements released in

connection with the proposal, however, have focused on departures from these standards in U.S.

implementation that are expected to increase capital requirements relative to the Basel Committee

framework and corresponding capital standards in other jurisdictions. For example, Federal Reserve

Chair Powell noted that the proposal “exceeds what is required by the Basel agreement, and exceeds as

well what we know of plans for implementation by other large jurisdictions,” citing in particular the inability

of U.S. banking organizations to use internal models for credit risk.

22

FDIC Vice Chairman Hill’s dissenting

statement identified various aspects of the proposal that he described as being “gold-plated” with respect

to (i.e., more stringent than) the Basel Committee standards and added that the agencies are “also

declining to make several modifications that European jurisdictions have proposed, each of which further

reinforces the relative conservatism of the U.S. approach.”

23

As an example, Vice Chairman Hill noted

that the proposal’s minimum haircut floors for securities financing transactions are not part of the

proposed implementation in the United Kingdom. Vice Chairman Hill’s further observed that the proposal

“rejects the notion of capital neutrality” previously expressed as a “goal” for implementing the Basel

Committee framework.

24

FDIC Director McKernan’s dissenting statement addressed various ways in

which the proposal differs from the Basel Committee framework and implementation in other jurisdictions,

in particular with respect to the following:

Investment grade corporate exposures: The proposal would require that, for a corporate

exposure to be eligible for the lower risk weight applicable to “investment grade” corporate

exposures, the company or its parent must have securities outstanding on a public securities

exchange, which FDIC Director McKernan noted have not been part of implementation in the

European Union and United Kingdom;

25

-4-

Basel III ‘Endgame’

August 1, 2023

Residential real estate and retail credit exposures: Risk weights for residential real estate and

retail credit exposures that are higher than those applicable under the Basel Committee

framework;

26

Exposures to small businesses, securities firms and banking organizations: The proposal

would not adopt reduced credit risk capital requirements “for exposures to small businesses,

securities firms and other nonbank financial institutions, or highly capitalized banking

organizations; or for short-term exposures to banking organizations;”

27

Internal loss multiplier: The internal loss multiplier for operational risk capital “would be floored

at one” whereas “[o]ther implementing authorities have set the internal loss multiplier equal to

one, as permitted by the Basel III standards;”

28

Default risk: Banking organizations “using the models-based measure for market risk would be

required to use the standardized approach for default-risk capital;”

29

Cash-funded credit-linked notes: Unlike the Basel Committee framework, the proposal does

not provide that “cash-funded credit-linked notes issued by a bank... that fulfill the criteria for

credit derivatives may be treated as cash-collateralized transactions;”

30

CVA exemption for commercial end-users: With respect to credit valuation adjustment

(“CVA”)

31

risk capital requirements, the proposal “would not include a tailored approach to

commercial end-users,” although “other implementing authorities have proposed a commercial

end-user exemption for CVA risk capital requirements;”

32

and

Securitization framework: The proposal “would not adopt the Basel III standards’ approach to

simple, transparent, and comparable securitizations.”

33

Federal Reserve Governor Waller’s dissenting statement addressed the interaction between the proposal

and the Federal Reserve’s stress testing framework and stress capital buffer requirement, noting that the

proposed increase in capital requirements “would be in large part driven by an increase in the capital

required for operational and market risks—risks that [the Federal Reserve has] already been capturing in

[its] stress testing for the past decade.”

34

Governor Waller added that the proposed revisions to the

market risk framework would “capture certain risks already accounted for in the [Federal Reserve’s] stress

test,” including the “market shock component of the stress test.”

35

Federal Reserve Governor Bowman warned of the proposal’s potential “detrimental impact on U.S.

market liquidity and lending” as well as the “punitive treatment for noninterest and fee-based income

through the proposed operational risk requirements.”

36

Federal Reserve Governors Waller and Bowman and FDIC Vice Chair Hill also expressed concern with

the proposed application of the same requirements for calculating regulatory capital and RWAs to

banking organizations in Categories I through IV.

37

B. GSIB Proposal

The Federal Reserve’s GSIB surcharge proposal

38

would calculate Method 2 surcharges based on

narrower score band ranges to reduce “cliff effects”

39

and require banking organizations to report values

based on an average daily or monthly basis, rather than as of a single date, to “reduce the effects of

temporary changes to indicator values around measurement dates.”

40

The proposal also would revise

-5-

Basel III ‘Endgame’

August 1, 2023

aspects of the calculation of “systemic indicators,” which serve as inputs both for the GSIB surcharge

calculation and for determining the capital, liquidity and other enhanced prudential standards applicable to

a banking organization under the tailoring framework adopted in 2019 to implement S. 2155.

41

The

Federal Reserve estimates that the proposed revisions to the systemic indicators would result in the

combined U.S. operations of seven foreign banking organizations (“FBOs”) and two U.S. intermediate

holding companies of FBOs (“IHCs”) becoming subject to Category II requirements.

42

Although the

proposal would retain the existing framework of the U.S. GSIB surcharge (which uses the higher of the

surcharges calculated under Method 1, based on the Basel Committee framework, and Method 2, which

is unique to the U.S.),

43

Governor Bowman suggested that the Federal Reserve “consider the impact of

the GSIB surcharge method two calculation, and whether it may discourage low-risk activities or result in

other unintended consequences” as well as “how the implementation of the US GSIB surcharge aligns

with other jurisdictions.”

44

The Federal Reserve estimates that the combined effect of the proposed revisions to the GSIB surcharge

would correspond to an aggregate increase in capital requirements of approximately $13 billion for

GSIBs.

45

An estimate of the combined aggregate effect of the Endgame proposal and GSIB surcharge

proposal was not provided.

KEY ELEMENTS OF THE PROPOSALS

The proposals, aggregating more than 1,150 pages, include a number of aspects that are highly complex

and technical. Below are several high-level observations regarding key elements of the proposals. In

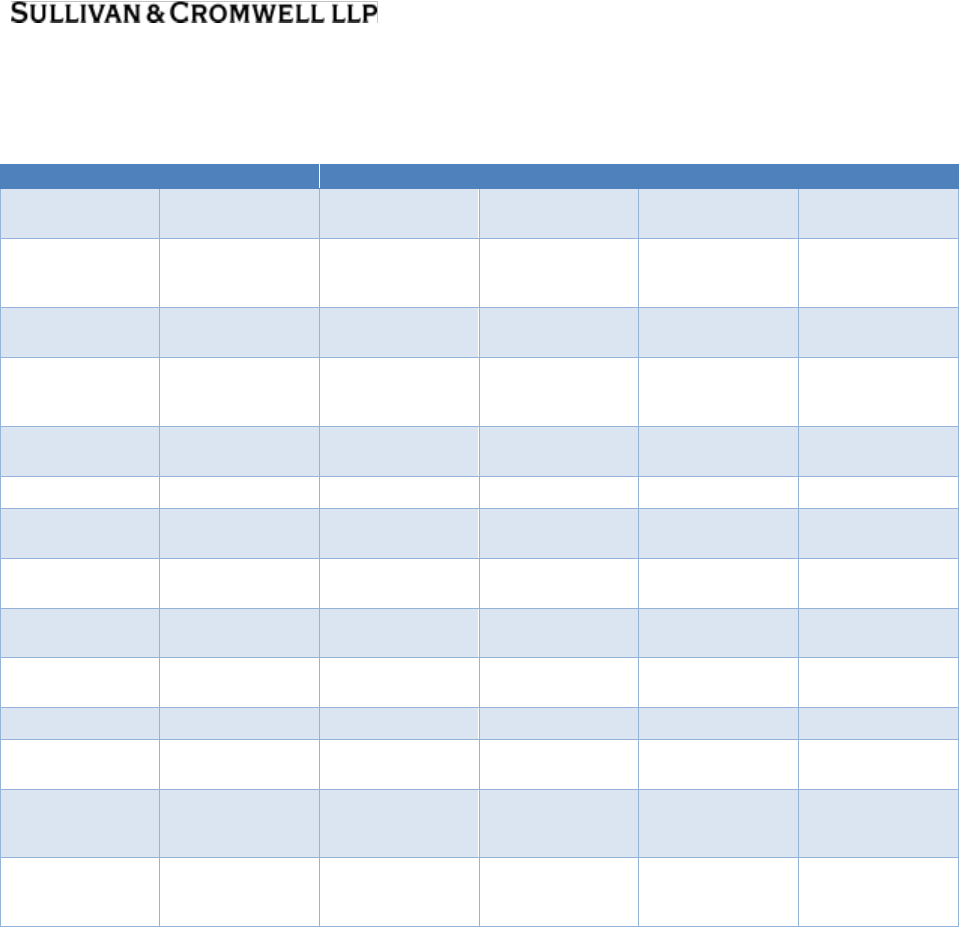

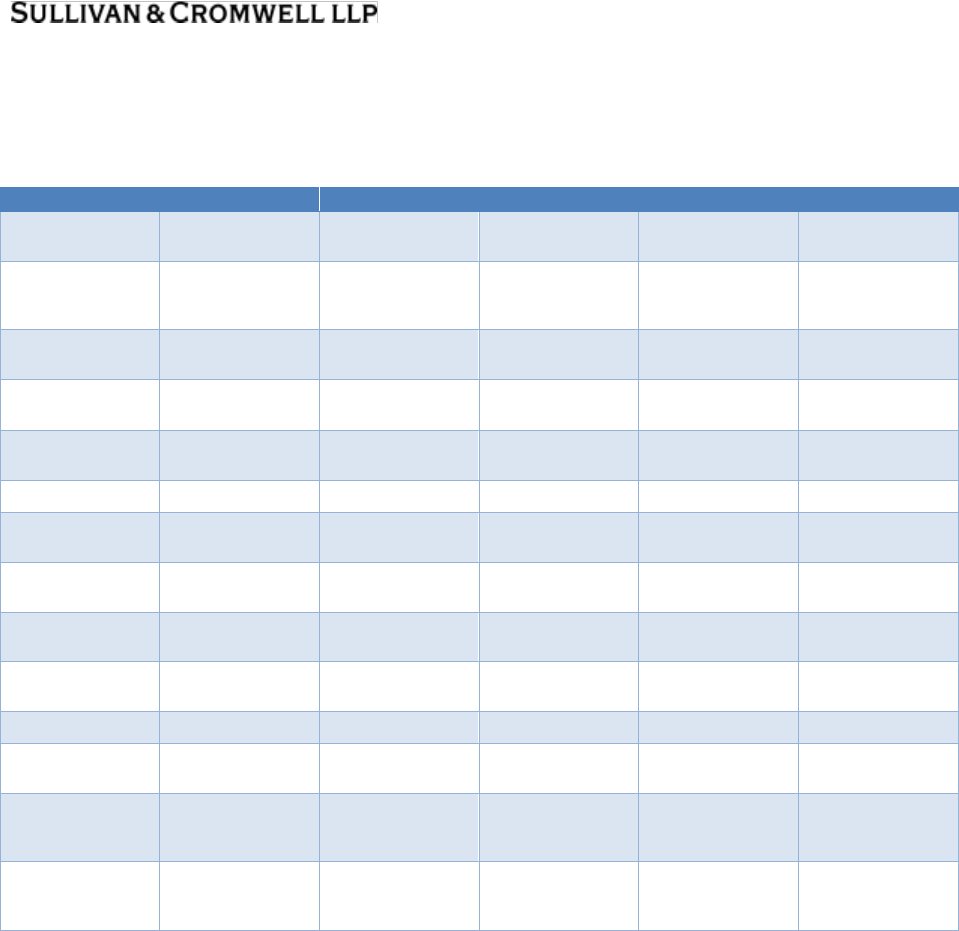

addition, Annex 1 provides a chart illustrating the current regulatory capital and related requirements

applicable to Category I through Category IV banking organizations and other banking organizations.

Annex 2 provides a chart illustrating the regulatory capital and related requirements that would apply

under the Endgame proposal.

Scope of application: The current “standardized approach”

46

under the regulatory capital rules

applies generally to U.S. banking organizations

47

and encompasses credit risk capital

requirements, which address exposures arising out of extensions of credit such as loans and debt

securities, derivatives, securities financing transactions and unsettled transactions, as well as off-

balance-sheet exposures such as commitments and guarantees, securitization exposures and

equity exposures. Banking organizations with trading assets plus trading liabilities in the

aggregate equal to (i) 10 percent or more of total assets or (ii) at least $1 billion currently must

also calculate market risk capital requirements.

In addition to calculating capital requirements under the generally applicable standardized

approach, U.S. GSIBs,

48

Category II banking organizations

49

and their insured depository

institution subsidiaries (generally, Category I and Category II organizations) also are subject to

the models-based advanced approaches capital rules, which encompass credit risk (including the

categories of credit risk referenced above), equity risk, operational risk, CVA risk and, for banking

organizations meeting the criteria for calculating market risk capital requirements described

above, market risk. The advanced approaches therefore incorporate two elements that are not

reflected in the current standardized approach: operational risk and CVA risk.

-6-

Basel III ‘Endgame’

August 1, 2023

Under the proposal, banking organizations with total consolidated assets of $100 billion or

more, including U.S. IHCs and depository institution subsidiaries of bank holding companies

with $100 billion or more in total consolidated assets, would be required to calculate capital

requirements using the revised credit risk, equity risk, operational risk, CVA risk and market

risk requirements implementing the revised Basel Committee standard (together, the

“Expanded Risk-Based Approach”).

The Expanded Risk-Based Approach with respect to credit risk and operational risk would

generally replace the current models-based advanced approaches in the capital rules and

would remove the option to use models with respect to equity risk.

With respect to market risk, all Category I through Category IV banking organizations would

calculate market risk capital requirements under the new market risk standard, which

includes a standardized measure and, subject to supervisory approval, a models-based

approach. For Category I through Category IV banking organizations, the proposal would not

include any threshold for applicability of the revised market risk capital requirements based

on the extent of a banking organization’s trading assets and liabilities.

In addition, banking organizations with trading assets plus trading liabilities in the aggregate

equal to (i) 10 percent or more of total assets or (ii) at least $5 billion also would be subject to

the revised market risk capital requirements.

The revised market risk capital requirements, based on the FRTB, would replace the market

risk framework currently in the capital rules, which is based on the July 2009 Basel market

risk capital standards (commonly referred to as “Basel II.5”).

50

With respect to CVA risk, Category I through Category IV banking organizations would

calculate CVA risk capital requirements using either a basic approach or, with supervisory

approval, a standardized measure. The proposal would eliminate the ability to use internal

models to calculate CVA risk capital requirements.

Collins Amendment and Output floor: Section 171 of the Dodd-Frank Wall Street Reform and

Consumer Protection Act (the “Dodd-Frank Act”), generally referred to as the “Collins

Amendment,” provides that the generally applicable capital requirements for banking

organizations (currently, the generally applicable standardized approach) must serve as a floor

for any banking organization’s capital requirements. Accordingly, a banking organization subject

to the advanced approaches currently is required to satisfy its minimum regulatory capital ratios

as calculated under both the generally applicable standardized approach and the advanced

approaches.

51

Under the proposal, a banking organization with $100 billion or more in total consolidated

assets would calculate its risk-based capital ratios under (i) the standardized approach capital

requirements—comprising both the standardized approach in Subpart D of the regulatory

capital rules and the revised market risk framework to implement the FRTB pursuant to the

proposal—and (ii) the revised credit risk, equity risk, operational risk, CVA risk and market

risk requirements calculated under the Expanded Risk-Based Approach. This structure

reflects the requirements of the Collins Amendment.

The calculation of RWAs under the Expanded Risk-Based Approach would be subject to an

output floor of 72.5 percent of the banking organization’s aggregate RWAs calculated based

on the approaches for credit risk, equity risk, operational risk and the standardized measure

for market risk. This output floor is compared to a banking organization’s aggregate RWAs

calculated based on the approaches for credit risk, equity risk, operational risk and market

risk (including models-based approaches, if applicable). The proposal provides that the

objective of an output floor would be “[t]o enhance the consistency of capital requirements

and ensure that the use of internal models for market risk does not result in unwarranted

reductions in capital requirements.”

52

Under the Basel Committee standard, a banking organization’s RWAs are equal to the higher

of (i) total RWAs calculated using the approaches the banking organization has supervisory

-7-

Basel III ‘Endgame’

August 1, 2023

approval to use (including models-based approaches for credit risk and market risk) and

(ii) 72.5 percent of total RWAs calculated under only the standardized approach with respect

to credit risk, counterparty credit risk, CVA risk, securitizations, market risk and operational

risk.

53

The Basel Committee noted that the output floor is applied “[t]o reduce excessive

variability of risk-weighted assets and to enhance the comparability of risk-weighted capital

ratios,” which “will ensure that banks’ capital requirements do not fall below a certain

percentage of capital requirements derived under standardized approaches.”

54

The banking organization’s risk-based capital ratios would be the lower of each ratio

calculated using RWAs under the standardized approach and the Expanded Risk-Based

Approach, taking into account the output floor for purposes of determining RWAs under the

Expanded Risk-Based Approach.

Capital conservation buffer: In addition to minimum capital requirements, banking organizations

also are subject to a capital conservation buffer requirement—which can be satisfied solely by

common equity tier 1 capital (“CET1”)—that imposes graduated constraints on distributions and

discretionary bonus payments if a banking organization does not satisfy the buffer requirement.

A Category I or Category II bank holding company or covered savings and loan holding company

calculates two buffers. For purposes of its standardized approaches capital conservation buffer,

the company adds its stress capital buffer requirement

55

to any applicable countercyclical capital

buffer

56

and GSIB surcharge.

57

For purposes of its advanced approaches capital ratios, it uses a

fixed 2.5 percent requirement instead of the stress capital buffer.

Bank holding companies and covered savings and loan holding companies that are not subject to

the advanced approaches and U.S. IHCs, in each case with total consolidated assets of at least

$100 billion, calculate only one buffer, either the stress capital buffer (if in Category IV) or adding

the stress capital buffer to any applicable countercyclical capital buffer (if in Category III).

58

For banking organizations that are not subject to the capital planning and stress capital buffer

requirements, including all insured depository institutions, the buffer is calculated as 2.5 percent

plus, if in Category I, Category II or Category III, any applicable countercyclical capital buffer.

Under the proposal, bank holding companies, covered savings and loan holding companies

and U.S. IHCs with total consolidated assets of at least $100 billion would be subject to a

single capital conservation buffer requirement that would include its stress capital buffer, in

addition to any applicable countercyclical capital buffer and GSIB surcharge. That capital

conservation buffer requirement would apply for purposes of calculating the banking

organization’s risk-based capital ratios under both the standardized approach and the

Expanded Risk-Based Approach.

The agencies stated that the “proposal mitigates potential competitive benefits for large

banking organizations first by requiring that they continue to be subject to [the] current

standardized approach,” noting that this “requirement guarantees that a large banking

organization covered by the proposal would maintain equity capital funding at a level at least

as high as that required by the U.S. standardized approach for a banking organization not

covered by the proposal.”

59

Stress testing and stress capital buffer: The Federal Reserve’s capital planning and stress

testing frameworks currently use only standardized approach RWAs for purposes of the Federal

Reserve’s supervisory stress tests and the determination of firms’ stress capital buffer

requirements.

Under the proposal, both the generally applicable standardized approach and the Expanded

Risk-Based Approach would be used in the Federal Reserve’s supervisory stress tests and

stress capital buffer calculations. A banking organization’s stress capital buffer requirement

would be calculated based on its “binding” CET1 capital ratio under the standardized

approach or the Expanded Risk-Based Approach.

-8-

Basel III ‘Endgame’

August 1, 2023

Relatedly, the proposal would require banking organizations subject to the Federal Reserve’s

capital planning and stress testing requirements to project risk-based capital ratios using the

calculation approach resulting in the binding capital ratios as of the start of the projection

horizon.

As reflected in the dissenting statement of Federal Reserve Governor Waller, the proposal

does not propose potential changes to the Federal Reserve’s supervisory stress tests or the

stress capital buffer requirement to reflect that certain risks that are currently addressed only

in the supervisory stress tests and therefore the stress capital buffer calculations through

projections of stressed losses would, as a result of the proposal, be addressed in both the

numerator of capital ratios through projections of stressed losses and the denominator of

capital ratios through the RWA calculations under the Expanded Risk-Based Approach,

particularly with respect to operational risk, CVA risk and, for firms subject to the global

market shock,

60

market risk arising out of “tail” events and market illiquidity.

61

AOCI opt-out election: Banking organizations that are not in Category I or Category II currently

are permitted to opt out of including all components of AOCI (excluding accumulated net gains

and losses on cash flow hedges for items not fair-valued on the balance sheet) in CET1. For firms

that have made this AOCI opt-out election, unrealized gains and losses on AFS debt securities do

not flow through regulatory capital.

62

Under the proposal, banking organizations with total consolidated assets of at least

$100 billion would not be permitted to continue to make this AOCI opt-out election. As a

result, Category III and Category IV banking organizations that have made an AOCI opt-out

election would be required to recognize, among other items, unrealized losses on AFS debt

securities in regulatory capital.

Category III and Category IV banking organizations would be subject to a phase-in period for

including AOCI components in CET1 beginning July 1, 2025 until June 30, 2028, with full

inclusion of required AOCI components starting July 1, 2028.

Deductions and minority interest framework: Banking organizations in Category I or Category

II currently are subject to more granular and complex deductions from regulatory capital than

banking organizations not subject to the advanced approaches. Since 2019, other banking

organizations, including those in Category III and Category IV, have applied a simplified

deduction framework.

63

Currently, a banking organization that is not subject to Category I or Category II capital standards

deducts its investments in the capital of unconsolidated financial institutions exceeding 25 percent

of CET1 (minus certain deductions and other adjustments to CET1), and also deducts from CET1

any amount of mortgage servicing assets (“MSAs”), temporary difference deferred tax assets

(“DTAs”) and investments in the capital of unconsolidated financial institutions individually

exceeding 25 percent of CET1.

In contrast, a banking organization subject to Category I or Category II capital standards deducts

from CET1 amounts of MSAs, temporary difference DTAs and significant investments in the

capital of unconsolidated financial institutions in the form of common stock both individually

exceeding 10 percent of CET1 and, in the aggregate and to the extent not deducted, exceeding

15 percent of CET1 (minus certain deductions and other adjustments to CET1). Category I and

Category II banking organizations also deduct their non-significant investments in the capital of

unconsolidated financial institutions that, in the aggregate and together with investments in

certain covered debt instruments qualifying for recognition under total loss-absorbing capacity

(“TLAC”) requirements, exceed 10 percent of CET1 (minus certain deductions and other

adjustments to CET1) and deduct significant investments in the capital of unconsolidated financial

institutions not in the form of common stock.

In addition, banking organizations not in Category I or Category II currently are subject to a

simpler methodology for calculating minority interest limitations than banking organizations in

Category I or Category II.

-9-

Basel III ‘Endgame’

August 1, 2023

Under the proposal, Category III and Category IV banking organizations would be subject to

the deductions framework and minority interest limitations that currently apply only to

Category I and Category II banking organizations.

Credit risk: Banking organizations currently calculate capital requirements for credit risk under

the standardized approach by assigning prescribed risk weights to exposures based on

applicable exposure classes and other characteristics within each exposure class. In addition,

banking organizations subject to the advanced approaches calculate credit risk capital

requirements under the advanced approaches using internal models pursuant to the advanced

internal ratings-based approach.

Elimination of internal models for credit risk: Under the proposal, banking organizations

would not be permitted to use internal models to calculate credit risk capital requirements. All

banking organizations would continue to calculate credit risk capital requirements using the

generally applicable standardized approach, and Category I through Category IV banking

organizations would also calculate credit risk capital requirements using the Expanded Risk-

Based Approach.

SA-CCR: Currently, a banking organization that is not subject to Category I or Category II

capital standards may use either the current exposure methodology (“CEM”) or the

standardized approach to counterparty credit risk (“SA-CCR”) to calculate the exposure

amount for OTC derivatives for purposes of risk-based capital ratios and the supplementary

leverage ratio. Banking organizations in Category I or Category II must use SA-CCR to

calculate the exposure amount for OTC derivatives for purposes of standardized approach

RWAs and the supplementary leverage ratio, and may use either SA-CCR or internal models

for purposes of advanced approaches RWAs.

Under the proposal, for purposes of RWAs calculated using both the Expanded Risk-Based

Approach and the generally applicable standardized approach and for purposes of the

supplementary leverage ratio, Category I through Category IV banking organizations would

be required to apply SA-CCR, with certain targeted revisions, and would not be permitted to

apply CEM to calculate the exposure amount for OTC derivatives. The proposal would

remove internal models as an available approach.

Credit risk mitigation: For purposes of the Expanded Risk-Based Approach, the proposal

would revise several aspects of the framework for recognizing the credit risk mitigation

benefits of certain types of guarantees, credit derivatives and collateral when calculating

RWAs, including with respect to:

Minimum haircut floors: There currently are no minimum haircut floors for securities

financing transactions under the U.S. capital rules.

Subject to specified exceptions, the proposal would implement minimum haircut floors for

margin loans or repo-style transactions in which a banking organization either lends cash

in exchange for securities or engages in certain collateral upgrade transactions with

“unregulated financial institutions,” which generally includes non-bank financial entities

that are not subject to prudential regulation.

Any transactions subject to the minimum haircut floors that do not meet the haircut floors

prescribed in the proposal would be required to be treated as unsecured exposures for

purposes of calculating capital requirements for credit risk (in other words, as if the

transaction were uncollateralized).

Supervisory haircuts: The proposal would increase certain of the supervisory haircuts

that currently apply to various categories of collateral.

Corporate debt securities: Under the proposal, a banking organization could recognize

a corporate debt security as an eligible credit risk mitigant only if the corporate issuer of

the debt security or its parent company has a publicly traded security outstanding.

-10-

Basel III ‘Endgame’

August 1, 2023

Master netting agreement: The proposal would incorporate a new formula that would

take into consideration the number of securities included in a netting set of eligible margin

loans or repo-style transactions.

General credit risk: For purposes of the Expanded Risk-Based Approach, the proposal

would establish new exposure classes and recalibrate risk weights for many existing

exposure classes under the generally applicable standardized approach, including with

respect to:

Unconditionally cancellable commitments: The credit conversion factor (“CCF”)

applicable to unconditionally cancellable commitments—which currently applies to

eligible exposures such as certain credit card lines and home equity lines of credit—

would increase to a 10 percent CCF from the 0 percent CCF that currently applies to

unconditionally cancellable commitments under the generally applicable standardized

approach.

Residential mortgage exposures: Under the generally applicable standardized

approach, many first-lien residential mortgage exposures currently qualify for a

50 percent risk weight.

64

For purposes of the Expanded Risk-Based Approach, the

proposal would increase risk weights for certain residential mortgage exposures with

higher loan-to-value ratios.

65

Exposures to banking organizations: The proposal would implement more granular

treatment for exposures to depository institutions and foreign banks based on a credit risk

assessment of the depository institution or foreign bank and the original maturity of the

exposure, which in some cases would result in higher risk weights for these exposures as

compared to the generally applicable standardized approach.

Corporate exposures: The proposal would incorporate a 65 percent risk weight with

respect to certain investment grade corporate exposures, in comparison to the 100

percent risk that currently applies to all corporate exposures under the generally

applicable standardized approach.

To qualify for the 65 percent risk weight under Expanded Risk-Based Approach, the

corporate entity or its parent company must have securities listed on a securities

exchange.

The proposal also would implement new categories of exposures for project finance

subject to specified risk weight treatment.

Retail exposures: The proposal would include exposure categories for certain types of

exposures to individuals or small businesses, which in some cases would result in lower

risk weights for exposures meeting specified criteria as compared to the current generally

applicable standardized approach.

The agencies discussed these risk weights and the risk weights for residential mortgage

exposures in the impact and economic analysis, noting that the “proposal attempts to

mitigate potential competitive effects between U.S. banking organizations by adjusting

the U.S. implementation of the Basel III reforms, specifically by raising the risk weights for

residential real estate and retail credit exposures.”

66

Securitizations: Category I and Category II banking organizations currently generally use

the Supervisory Formula Approach (“SFA”) for purposes of calculating RWA amounts for

securitization exposures for purposes of the advanced approaches.

The proposal would eliminate the SFA and replace it with the securitization standardized

approach (called the “SEC-SA”), a modified version of the Standardized Supervisory Formula

Approach (often referred to as the “SSFA”) provided in the current version of the

standardized approach.

-11-

Basel III ‘Endgame’

August 1, 2023

Equity exposures: Category I and Category II banking organizations currently may calculate

RWA amounts for equity exposures under either a simple risk-weight approach or, with

supervisory approval, using internal models.

The proposal would eliminate the model-based approach for equity exposures and

incorporate targeted revisions to the simple risk-weight approach, including removing the 100

percent risk weight for non-significant equity exposures, eliminating the effective and

ineffective hedge pair treatment, and increasing the risk weight for equity exposures to

certain investment firms with greater than immaterial leverage from 600 percent to 1,250

percent.

Cash-funded credit-linked notes: Under the Basel Committee standard, cash proceeds

received in connection with the issuance of credit-linked notes may qualify as eligible

financial collateral under the framework for recognizing eligible credit risk mitigants.

67

The

U.S. capital rules currently do not include a similar provision.

The proposal does not address the treatment of credit-linked notes with respect to the

standardized approach or the Expanded Risk-Based Approach.

Operational risk: The capital requirements for operational risk currently apply only to Category I

and Category II banking organizations and only for purposes of advanced approaches RWAs.

Category I and Category II banking organizations currently use the advanced measurement

approaches (“AMA”), which use a banking organization’s internal operational risk models to

calculate risk-based capital requirements for operational risk.

Scope and application: Under the proposal, Category I through Category IV banking

organizations would be required to calculate capital requirements for operational risk for

purposes of RWAs calculated under the Expanded Risk-Based Approach. As a result,

Category III and Category IV banking organizations, which are not currently subject to the

advanced approaches, would become subject to operational risk capital requirements.

Operational risk capital requirements would not, however, be added to the generally

applicable standardized approach. Additionally, the proposal would replace the AMA with the

standardized measurement approach (“SMA”).

SMA calculation: The SMA is not based on a banking organization’s models and instead

generally calculates operational risk capital requirements based on a banking organization’s

income, expenses, interest-earning assets and historical losses, using Business Indicator

(“BI”), Business Indicator Component (“BIC”) and Internal Loss Multiplier (“ILM”) calculations.

A banking organization calculates its BI using income statement and balance sheet items and

the BIC is determined by multiplying the BI by prescribed marginal coefficients that increase

based on the BI calculation.

BI calculation: Under the proposal, the BI would consist of (i) an interest, leases and

dividend component, (ii) a services component and (iii) a financial component. With respect

to the interest, leases and dividend component, the input for net interest income would be

subject to a cap of 2.25 percent of interest-earning assets.

ILM calculation: ILM is a function of the banking organization’s BIC and its Loss Component

(“LC”).

The LC is equal to 15 times the average annual operational risk losses the banking

organization incurred over the previous ten years.

When the LC is greater than the BIC, the ILM is greater than one, which results in higher

operational risk capital requirements reflecting the incorporation of historical internal losses.

The proposal would not set the ILM at a value of one, which is permitted at national discretion

under the Basel Committee standard. As a result, under the proposal, historical operational

risk losses would be relevant in calculating operational risk capital requirements. In addition,

the proposal would incorporate a floor of one for the ILM.

-12-

Basel III ‘Endgame’

August 1, 2023

Market risk: Banking organizations with trading assets plus trading liabilities in the aggregate

equal to 10 percent or more of total assets or at least $1 billion are currently required to calculate

market risk capital requirements under the U.S. capital rules.

Banking organizations subject to the advanced approaches that meet the criteria for calculating

market risk capital requirements also calculate an advanced measure for market risk that is

substantially similar to the standardized approach for market risk.

Market risk capital requirements currently apply generally to “covered positions” as defined under

the U.S. capital rules.

A banking organization calculating market risk capital requirements under the standardized

approach or the advanced approaches generally applies an internal model-based approach,

pursuant to which the banking organization uses an internal Value-at-Risk (“VaR”) model subject

to supervisory approval that is calibrated to a 99 percent confidence level and a holding period of

ten business days. Additional aspects of market risk capital requirements, such as specific risk,

are captured using either models or standardized approaches.

Scope: All Category I through Category IV banking organizations would be required to

calculate market risk capital requirements. In addition, banking organizations with trading

assets plus trading liabilities in the aggregate equal to (i) 10 percent or more of total assets or

(ii) at least $5 billion also would be subject to the revised market risk capital requirements.

The proposal would replace the current market risk capital standard based on the Basel II.5

framework with the FRTB standard.

Market risk boundary: The proposal would revise the criteria for determining whether a

position is subject to market risk capital requirements and include a list of instruments that

are presumptively subject to market risk or are subject to non-market risk capital

requirements.

The proposal also would implement a capital “add-on” when a banking organization

reclassifies an instrument after initial designation of the instrument as being subject to market

risk capital requirements or non-market risk capital requirements.

Standardized approach: The U.S. capital rules currently include only the models-based

requirements for market risk under the Basel II.5 framework and do not include the Basel

Committee’s standardized approach.

The proposal would implement a new standardized approach for market risk consisting of

three components: (i) a Sensitivity-Based Approach (“SBA”) capital requirement, (ii) a default

risk capital (“DRC”) requirement that generally applies to debt instruments, equity instruments

and securitizations and (iii) a residual risk add-on capital requirement designed to address

risks that may not be covered sufficiently under the SBA or DRC.

In broad terms, under the SBA, a banking organization would calculate the sensitivities of

instruments subject to market risk capital requirements to delta risk,

68

vega risk

69

and

curvature risk

70

in respect of prescribed risk classes.

71

Models-based approach: The proposal would revise the internal model-based approach to

introduce more stringent requirements for using models to calculate market risk capital

requirements.

A banking organization must receive supervisory approval to use models by individual trading

desk and would be subject to both (i) a profit and loss attribution (“PLA”) test and

(ii) backtesting requirements, in comparison to the current approach that applies the modeling

requirements on an entity-wide basis and does not include an explicit PLA test.

A banking organization that does not satisfy these requirements must apply the standardized

approach.

In addition, for certain exposures such as securitization positions and certain equity positions

in investment funds, internal models would not be permitted and a banking organization

-13-

Basel III ‘Endgame’

August 1, 2023

would be required to calculate market risk capital requirements for these exposures under the

standardized approach for purposes of calculating RWAs under both the generally applicable

standardized approach and Expanded Risk-Based Approach.

A banking organization calculating market risk capital requirements under the internal

models-based approach would use an expected shortfall method calibrated at a 97.5

percent level in lieu of the current requirement to calculate VaR calibrated at a 99 percent

level. In addition, instead of a static 10-day holding period currently employed under the

market risk capital rules, the proposal would implement more granular liquidity horizons.

Under the proposal, non-modellable risk factors (in other words, exposures that do not

satisfy the criteria for internal models) are subject to separate capital requirements.

Disclosure: The proposal would make certain targeted revisions to the existing disclosure

requirements with respect to market risk capital requirements, including quantitative

disclosure requirements that would apply to banking organizations using the models-based

measure and qualitative disclosure regarding processes and policies for managing market

risk.

CVA risk: Under the U.S. capital rules, capital requirements for CVA risk currently apply only to

banking organizations subject to the advanced approaches and only for purposes of calculating

advanced approaches RWAs. A banking organization may calculate CVA risk using either a

simple CVA approach or, with prior supervisory approval, the advanced CVA approach that uses

an internal model.

Scope: Under the proposal, Category I through Category IV banking organizations would be

required to calculate capital requirements for CVA risk for purposes of RWAs calculated

under the Expanded Risk-Based Approach. As a result, Category III and Category IV banking

organizations, which are not currently subject to the advanced approaches, would become

subject to CVA risk capital requirements. CVA risk capital requirements would not be added

to the generally applicable standardized approach.

Application: The proposal would eliminate the internal models approach to calculate capital

requirements for CVA risk. Instead, under the proposal, a banking organization required to

calculate capital requirements for CVA risk would use the basic approach or, with supervisory

approval, the standardized approach.

The standardized approach for CVA risk has broad conceptual similarity with the

proposed revised market risk capital framework to implement the FRTB, in that banking

organizations calculate capital requirements for delta risk and vega risk across prescribed

risk types.

Disclosure: In addition to the revisions to market risk disclosures described above, the proposal

would revise existing qualitative disclosure requirements and introduce new and enhanced

qualitative disclosure requirements. The proposal also generally would move many of the existing

public quantitative disclosure to regulatory reporting forms through separate proposals.

The proposal also provides that “[t]he agencies are planning to separately propose modifications

to the FFIEC 101 report so that all inputs to the business indicator” and “total net operational

losses…would be publicly reported as separate inputs to the applicable calculations.”

72

Implementation and transitional arrangements: The proposal would take effect beginning

July 1, 2025. On that date, a banking organization would phase in its RWAs calculated under the

Expanded Risk-Based Approach at 80 percent, with the Expanded Risk-Based Approach fully

phased in beginning July 1, 2028. From July 1, 2025 through July 1, 2028, Category III and

Category IV banking organizations that had made an AOCI opt-out election would phase in AOCI

into its calculation of regulatory capital. The proposal would not include a transition period with

respect to including the revised capital requirements for market risk to the calculation of RWAs

under the standardized approach.

-14-

Basel III ‘Endgame’

August 1, 2023

Under the Basel Committee standard, in contrast, the output floor is phased in beginning at

50 percent on January 1, 2023 to 72.5 percent beginning January 1, 2028. During the phase-

in period, national authorities are permitted to cap at 25 percent of a banking organization’s

RWAs the incremental increase in total RWAs resulting from the application of the output

floor.

Leverage ratio: The Basel Committee’s December 2017 standard introduces a leverage ratio

buffer applicable to all GSIBs in an amount equal to 50 percent of the applicable GSIB surcharge.

Under the proposal, Category IV banking organizations would become subject to the

supplementary leverage ratio. The proposal would not revise the current scope or application of

the enhanced supplementary leverage ratio under the U.S. capital rules, including the

supplementary leverage ratio buffer that currently applies to U.S. GSIBs.

73

Countercyclical capital buffer: The countercyclical capital buffer currently applies to Category I,

Category II and Category III banking organizations.

Under the proposal, Category IV banking organizations would become subject to the

countercyclical capital buffer.

GSIB surcharge: The Federal Reserve also proposed to revise targeted elements of the GSIB

surcharge that currently applies to U.S. GSIBs.

74

A GSIB currently must calculate its GSIB surcharge under Method 1 and Method 2. Under

the GSIB proposal, to reduce “cliff effects,” Method 2 would be revised such that a 20-basis-

point increase would correspond to a 0.1-percentage-point increase in the GSIB surcharge, in

lieu of the 0.5-percentage-point increase that currently corresponds to 100-basis point

increases in Method 2 scores. The proposal would not implement similar revisions to the

Method 1 calculation.

The proposal would amend the calculation of systemic indicators currently measured as of a

year-end to calculate the indicators on an average basis over a full year.

The Federal Reserve requests comment regarding potential modifications to the effective

date of changes to the GSIB surcharge requirement following changes to a banking

organization’s GSIB score. The proposal would clarify that the GSIB surcharge for a calendar

year is the surcharge calculated in the immediately prior calendar year unless the surcharge

calculated in the calendar year two years prior was lower, in which case the GSIB surcharge

calculated in the calendar year two years prior would be operative.

The proposal would amend aspects of the Systemic Risk Report (FR Y-15). Notably, the

proposal would revise the systemic indicator with respect to cross-jurisdictional activity to

include derivatives. The interconnectedness and complexity systemic indicators also would

be revised to include a banking organization’s exposure to its client with respect to client-

cleared derivative positions under the “agency” clearing model in the U.S.

The proposal indicates that the proposed changes to the cross-jurisdictional activity systemic

indicator in the aggregate would result in seven FBOs that are currently subject to Category

III or Category IV standards becoming subject to Category II standards and two U.S. IHCs

subject to Category III standards becoming subject to Category II standards.

75

As noted in the proposal, the combined U.S. operations of these FBOs would become subject

to more stringent capital and liquidity requirements, including (i) daily liquidity reporting

(rather than monthly or no liquidity reporting), (ii) monthly internal liquidity stress testing

(rather than quarterly) and (iii) full liquidity risk management requirements (rather than

reduced). The U.S. IHCs becoming subject to Category II standards would be required to

conduct annual company-run stress testing (rather than every two years) and meet the full

liquidity coverage ratio and net stable funding ratio requirements, rather than a reduced 85

percent requirement.

-15-

Basel III ‘Endgame’

August 1, 2023

The proposed changes to the GSIB surcharge and FR Y-15 reporting form would take effect

two calendar quarters after the date of adoption of a final rule.

* * *

Copyright © Sullivan & Cromwell LLP 2023

-16-

Basel III ‘Endgame’

August 1, 2023

ENDNOTES

1

Federal Reserve, FDIC, OCC, Regulatory capital rule: Amendments applicable to large banking

organizations and to banking organizations with significant trading activity (July 27, 2023),

available at https://www.federalreserve.gov/aboutthefed/boardmeetings/frn-basel-iii-20230727.pdf

(“Endgame proposal”).

2

Vice Chair Barr noted that “One can think of the proposal’s more accurate risk measures as

equivalent to requiring the largest banks [to] hold an additional 2 percentage points of capital, or

an additional $2 of capital for every $100 of risk-weighted assets.” Michael S. Barr, Holistic

Capital Review, Remarks at the Bipartisan Policy Center (July 10, 2023), available at

https://www.federalreserve.gov/newsevents/speech/files/barr20230710a.pdf (“Barr Holistic

Capital Review”).

3

Endgame proposal p. 492.

4

Basel Committee, Basel III: Finalising Post-Crisis Reforms (Dec. 2017), available at

https://www.bis.org/bcbs/publ/d424.pdf. The Basel III Endgame reforms are discussed in Basel

Committee Releases Standards to Finalize Basel III Framework, Sullivan & Cromwell (Dec. 19,

2017), available at https://www.sullcrom.com/SullivanCromwell/_Assets/PDFs/Memos/SC_

Publication_Bank_Capital_Requirements_12192017.pdf.

5

Basel Committee, Minimum Capital Requirements for Market Risk (rev. Feb. 2019), available at

https://www.bis.org/bcbs/publ/d457.pdf.

6

Federal Reserve, Regulatory Capital Rule: Risk-Based Capital Surcharges for Global

Systemically Important Bank Holding Companies; Systemic Risk Report (FR Y-15) (July 27,

2023), available at https://www.federalreserve.gov/aboutthefed/boardmeetings/frn-gsib-

20230727.pdf (“GSIB surcharge proposal”).

7

Barr Holistic Capital Review.

8

Barr Holistic Capital Review.

9

On July 12, 2023, the American Bankers Association, the Bank Policy Institute, the Financial

Services Forum, the Institute for International Bankers and the Securities Industry and Financial

Markets Association submitted a letter requesting a 120-day comment period. See Letter to

Chair Jerome H. Powell, Board of Governors of the Federal Reserve System (July 12, 2023),

available at https://bpi.com/wp-content/uploads/2023/07/Joint-Trades-Letter-to-Chair-Powell-7-

12-23-.pdf.

10

To the extent recognized in AOCI, unrealized gains and losses on held-to-maturity (“HTM”) debt

securities would also flow through regulatory capital.

11

Endgame proposal p. 489.

12

Endgame proposal p. 489.

13

Jerome H. Powell, Statement by Chair Jerome H. Powell (July 27, 2023), available at

https://www.federalreserve.gov/newsevents/pressreleases/powell-statement-20230727.htm

(“Powell Opening Statement”).

14

Powell Opening Statement.

15

Federal Reserve Board, Open Board Meeting on July 27, 2023, available at

https://www.federalreserve.gov/aboutthefed/boardmeetings/20230727open.htm.

16

Endgame proposal p. 489.

17

Staff Memorandum to the Board of Governors (July 18, 2023), available at

https://www.federalreserve.gov/aboutthefed/boardmeetings/gsib-memo-20230727.pdf.

18

Powell Opening Statement.

-17-

Basel III ‘Endgame’

August 1, 2023

ENDNOTES (CONTINUED)

19

Endgame proposal p. 495. See also Michael Barr, Opening Statement on the Large Bank Capital

Requirement Proposal by Vice Chair for Supervision Michael S. Barr (July 27, 2023), available at

https://www.federalreserve.gov/newsevents/pressreleases/barr-statement-20230727.htm (“Barr

Opening Statement”).

20

Barr Opening Statement.

21

Endgame proposal p. 2.

22

Powell Opening Statement.

23

Travis Hill, Statement by Travis Hill, Vice Chairman, FDIC, on the Proposal to Revise the

Regulatory Capital Requirements for Large Banks (July 27, 2023), available at

https://www.fdic.gov/news/speeches/2023/spjul2723b.html (“Hill Dissenting Statement”).

24

Hill Dissenting Statement. Randal Quarles, the former Vice Chair for Supervision of the Federal

Reserve, noted a broad preference for neutrality in capital levels. Randal K. Quarles, Between

the Hither and Farther Shore: Thoughts on Unfinished Business, Remarks at the American

Enterprise Institute (Dec. 2, 2021) (“A major issue that we are grappling with is how to implement

these reforms, which reduce the role of bank internal models on bank capital requirements, while

maintaining the overall level of aggregate capital requirements…What policymakers will need to

do as they implement the Basel III reforms is determine whether adjustments to other parts of the

capital framework are necessary to ensure that we do not unduly increase the level of required

capital in the system.”), available at https://www.federalreserve.gov/newsevents/speech/quarles

20211202a.htm.

25

Jonathan McKernan, Statement by Jonathan McKernan, Member, FDIC Board of Directors, on

the Proposed Amendments to the Capital Framework (July 27, 2023), available at

https://www.fdic.gov/news/speeches/2023/spjul2723c.html (“McKernan Dissenting Statement”)

(“To be eligible for the reduced credit-risk-capital requirement for investment-grade corporate

exposures, the company (or its parent) must have securities outstanding on a recognized

securities exchange. The Basel Committee has offered no rationale for concluding that having a

publicly listed security correlates strongly with a company’s capacity to meet financial

commitments. Understandably, the European Union and United Kingdom regulators’

implementation proposals have dropped the concept. Our proposal keeps it, but is stuck offering

only a cursory rationale.”).

26

McKernan Dissenting Statement (“The expanded risk-based approach would increase the Basel

III risk weights for residential real estate exposures (by 20 percentage points), other real estate

exposures not dependent on cash flows generated by the real estate (by 25 percentage points for

exposures to individuals, 15 percentage points for exposures to small- or medium-sized entities

(‘SMEs’)), and retail exposures (by 10 percentage points) to ensure competitive parity between

the large banking organizations covered by this proposal and the smaller banking organizations

that are not.”).

27

McKernan Dissenting Statement.

28

McKernan Dissenting Statement.

29

McKernan Dissenting Statement.

30

McKernan Dissenting Statement.

31

CVA generally relates to potential changes in the value of derivative instruments as a result of the

deterioration in the creditworthiness of a counterparty.

32

McKernan Dissenting Statement.

33

McKernan Dissenting Statement.

-18-

Basel III ‘Endgame’

August 1, 2023

ENDNOTES (CONTINUED)

34

Christopher J. Waller, Statement on Large Bank Capital Requirement Proposals by Governor

Christopher J. Waller (July 27, 2023), available at https://www.federalreserve.gov/aboutthefed/

boardmeetings/waller-statement-20230727.pdf (“Waller Dissenting Statement”).

35

Waller Dissenting Statement.

36

Michelle W. Bowman, Statement by Governor Michelle W. Bowman At the Board Meeting

considering proposed rules to implement the Basel III endgame agreement for large banks and

adjustments to the surcharge for U.S. global systemically important banks (July 27, 2023),

available at https://www.federalreserve.gov/aboutthefed/boardmeetings/bowman-statement-

20230727.pdf (“Bowman Dissenting Statement”).

37

Waller Dissenting Statement (“Finally, as this proposal applies to all firms with more than $100

billion in assets, I am concerned that we are headed down a road where we would be no longer in

compliance with section 165 of the Dodd-Frank Act, as amended by the Economic Growth,

Regulatory Relief, and Consumer Protection Act, which mandates tailoring for firms above $100

billion in assets and provides that firms with between $100 billion and $250 billion in assets are

not subject to enhanced prudential standards unless a standard is affirmatively applied to such

firms based on specific factors set out by Congress. It is unclear to me whether this proposal

meets that statutory bar.”); Bowman Dissenting Statement (“I am also concerned that today’s

proposal moves one step closer to eliminating the tailoring required by S. 2155 from the

prudential capital framework.”); Hill Dissenting Statement (“For purposes of the capital rules, the

proposal effectively collapses Categories II, III, and IV into one category. The proposal undoes

almost all of the tailoring of the capital framework for large banks, and is a repudiation of the

intent and spirit of S. 2155.”).

38

The GSIB surcharge is currently codified in 12 C.F.R. Part 217, Subpart H.

39

GSIB proposal p. 15.

40

GSIB proposal p. 1.

41

The tailoring framework is discussed in Regulatory Tailoring for Large Domestic and Foreign

Banking Organizations, Sullivan & Cromwell (Oct. 18, 2019), available at

https://www.sullcrom.com/SullivanCromwell/_Assets/PDFs/Memos/SC-Publication-Banking-

Agencies-Finalize-Tailoring-of-Enhanced-Prudential-Standards-and-Capital-and-Liquidity-

Requirements.pdf.

42

GSIB proposal pp. 46-47.

43

The GSIB surcharge is discussed in Bank Capital Requirements: Federal Reserve Board

Approves Final Common Equity Surcharge For U.S. Global Systemically Important Banks (July

29, 2015), available at https://www.sullcrom.com/SullivanCromwell/_Assets/PDFs/Memos/SC-

GSIB-Surcharge-Memo.pdf.

44

Bowman Dissenting Statement.

45

GSIB proposal p. 45.

46

The current standardized approach is codified in Subpart D of the agencies’ regulatory capital

rules and applies generally to banking organizations subject to U.S. regulatory capital

requirements.

47

For these purposes, banking organizations refer to the scope of entities subject to the U.S.

regulatory capital rules, including U.S. bank holding companies, covered savings and loan

holding companies, state-chartered banks and national banks, state savings associations and

federal savings associations and U.S. IHCs of FBOs established under the Federal Reserve’s

Regulation YY. In addition to the generally applicable regulatory capital rules, insured depository

institutions also are separately subject to the agencies’ prompt corrective action framework under

Section 38 of the Federal Deposit Insurance Act. 12 U.S.C. § 1831o.

-19-

Basel III ‘Endgame’

August 1, 2023

ENDNOTES (CONTINUED)

48

Under Section 252.5(b) of the Federal Reserve’s Regulation YY, a banking organization is a

GSIB if it is identified as a GSIB pursuant to 12 C.F.R. § 217.402.

49

Under Section 252.5(c) of the Federal Reserve’s Regulation YY, a U.S. bank holding company or

U.S. IHC is a Category II banking organization if it is not a GSIB and has (A) $700 billion or more

in average total consolidated assets; or (B) (1) $75 billion or more in average cross-jurisdictional

activity; and (2) $100 billion or more in average total consolidated assets. With respect to a U.S.

IHC that is a Category II banking organization pursuant to these criteria, although a U.S. IHC

generally must comply with the Federal Reserve’s regulatory capital rules in the same manner as

a bank holding company, a U.S. IHC is not required to calculate RWAs and capital ratios using

the models-based advanced approaches. 12 C.F.R. § 252.153(e)(1)(i)(A).

50

Basel Committee on Banking Supervision, Revisions to the Basel II Market Risk Framework (July

2009), available at https://www.bis.org/publ/bcbs158.pdf.

51

Under Section 171 of the Dodd-Frank Act, the minimum risk-based capital and leverage

requirements established by the agencies under Section 171 may not be less than the generally

applicable risk-based capital and leverage requirements under the prompt corrective action

framework. 12 U.S.C. § 5371. The agencies have indicated that Section 171 of the Dodd-Frank

Act applies only with respect to the minimum requirements, and does not apply to the capital

conservation buffer. The 2012 interagency proposal to implement Basel III notes that, for

purposes of the capital conservation buffer, a banking organization would use standardized total

RWAs if the banking organization is subject to the standardized approach and advanced total

RWAs if the banking organization is subject to the advanced approaches. Regulatory Capital

Rules: Regulatory Capital, Implementation of Basel III, Minimum Regulatory Capital Ratios,

Capital Adequacy, Transition Provisions, and Prompt Corrective Action, 77 Fed. Reg. 52,792,

52,803, footnote 33 (Aug. 30, 2012) (proposed rule). The 2013 final rule to implement Basel III

issued by the Federal Reserve and the OCC provides that a banking organization subject to the

advanced approaches use its “risk-based capital ratios under section 10 of the final rule (that is,

the lesser of the standardized and the advanced approaches ratios) as the basis for calculating

their capital conservation buffer (and any applicable countercyclical capital buffer). The agencies

believe such an approach is appropriate because it is consistent with how advanced approaches

banking organizations compute their minimum risk-based capital ratios.” See Regulatory Capital

Rules: Regulatory Capital, Implementation of Basel III, Capital Adequacy, Transition Provisions,

Prompt Corrective Action, Standardized Approach for Risk-Weighted Assets, Market Discipline

and Disclosure Requirements, Advanced Approaches Risk-Based Capital Rule and Market Risk

Capital Rule, 78 Fed. Reg. 62,018, 62,036 (Oct. 11, 2013)

52

Endgame Proposal p. 24.

53

Basel Committee on Banking Supervision, Calculation of minimum risk-based capital

requirements, paragraph 20.4 (effective Jan. 1, 2023).

54

Basel Committee on Banking Supervision, Basel III: Finalizing post-crisis reforms, p. 137 (Dec.

2017), available at https://www.bis.org/bcbs/publ/d424.pdf.

55

A banking organization’s stress capital buffer is determined from the results of the Federal

Reserve’s supervisory stress test. Subject to a floor of 2.5 percent, the stress capital buffer is

equal to (i) the ratio of the bank holding company’s CET1 to RWAs calculated under the

standardized approach as of the final quarter of the prior capital plan cycle, minus (ii) the lowest

project ratio of CET1 to RWAs calculated under the standardized approach in any quarter of the

planning horizon under a supervisory stress test, plus (iii) the ratio of (1) the sum of planned

common stock dividends for each of the fourth through seventh quarters of the planning horizon

to (2) RWAs in the quarter in which the bank holding company had its lowest projected ratio of

CET1 to RWAs calculated under the standardized approach in any quarter of the planning

horizon under a supervisory stress test. 12 C.F.R. § 225.8(f)(2).

-20-

Basel III ‘Endgame’

August 1, 2023

ENDNOTES (CONTINUED)

For a bank holding company that is not a Category IV bank holding company, the Federal

Reserve calculates the stress capital buffer annually. In general, for a Category IV bank holding

company, as defined in Section 252.5(e) of the Federal Reserve’s Regulation YY, the Federal

Reserve calculates the bank holding company’s stress capital buffer requirement biennially,

occurring in each calendar year ending in an even number, and adjusts the stress capital buffer

requirement biennially in each calendar year ending in an odd number based on the planned

dividends in the company’s capital plan submission. 12 C.F.R. § 225.8(f)(1). A U.S. bank holding

company or U.S. IHC is a Category IV banking organization if it has average total consolidated

assets of at least $100 billion and is not a GSIB, Category II banking organization or Category III

banking organization.

56

Banking organizations subject to the advanced approaches and Category III banking

organizations are required to calculate a countercyclical capital buffer amount. Under Section

252.5(d) of the Federal Reserve’s Regulation YY, a U.S. bank holding company or U.S. IHC is a

Category III banking organization if it is neither a Category I nor a Category II banking

organization and has either at least $250 billion in average total consolidated assets or $100

billion in average total consolidated assets and at least $75 billion in average total nonbank

assets, average weighted short-term wholesale funding or average off-balance-sheet exposure.

57

A bank holding company is a GSIB subject to the GSIB surcharge if its Method 1 score, as

calculated under 12 C.F.R. § 217.404, equals or exceeds 130 basis points.

58

The Federal Reserve’s capital planning and stress capital buffer requirement applies to top-tier

U.S. bank holding companies and U.S. covered savings and loan holding companies with at least

$100 billion in total consolidated assets and to U.S. IHCs with total consolidated assets of at least

$100 billion established by an FBO pursuant to Section 252.153 of Regulation YY. 12 C.F.R. §

225.8(b), 12 C.F.R. § 238.170(b)(1).

59

Endgame proposal p. 499.

60

The global market shock scenario “is a set of hypothetical shocks to a large set of risk factors

reflecting general market distress and heightened uncertainty…The global market shock affects

the mark-to-market value of trading positions and counterparty credit losses in the first quarter of

the scenario.” Federal Reserve, 2023 Stress Test Scenarios, pp. 8-9 (Feb. 2023), available at

https://www.federalreserve.gov/newsevents/pressreleases/files/bcreg20230209a1.pdf. The

global market shock scenario applies to Category I, Category II and Category III banking

organizations with aggregate trading assets and liabilities of at least $50 billion, or trading assets

and liabilities of at least 10 percent of total consolidated assets. 12 C.F.R. § 252.54(b)(2)(i).

61

The Federal Reserve’s 2023 stress test methodology provides the following with respect to the

global market shock: “The trading and private equity model covers a wide range of firms’

exposures to asset classes such as public equity, foreign exchange, interest rates, commodities,

securitized products, traded credit (e.g., municipals, auction rate securities, corporate credit, and

sovereign credit), private equity, and other fair-value assets. Loss projections are constructed by

applying movements specified in the global market shock scenario to market values of firm-

provided positions and risk factor sensitivities. In addition, the global market shock is applied to

firm counterparty exposures to generate losses due to changes in CVA.” Federal Reserve, 2023

Stress Test Methodology, p. 14 (June 2023) (footnote text omitted), available at

https://www.federalreserve.gov/publications/files/2023-june-supervisory-stress-test-

methodology.pdf.

62

Substantially all Category III and Category IV banking organizations have made this AOCI opt-out

election. In addition, to the extent recognized in AOCI, unrealized gains and losses on HTM debt

securities also do not flow through regulatory capital.

63

Regulatory Capital Rule: Simplifications to the Capital Rule Pursuant to the Economic Growth and

Regulatory Paperwork Reduction Act of 1996, 84 Fed. Reg. 35,234 (July 22, 2019).

-21-

Basel III ‘Endgame’

August 1, 2023

ENDNOTES (CONTINUED)

64

A first-lien residential mortgage exposure qualifies for a 50 percent risk weight if it (i) is secured

by a property that is either owner-occupied or rented; (ii) is made in accordance with prudent

underwriting standards, including relating to the loan amount as a percent of the appraised value

of the property; (iii) is not 90 days or more past due or carried in nonaccrual status; and (iv) is not

restructured or modified.

65

The agencies note that they “are supportive of home ownership and do not intend the proposal to

have a disparate impact on home affordability or homeownership opportunities, including for low-

and moderate-income (LMI) home buyers or other historically underserved markets” and that they

“are particularly interested in whether the proposed framework for regulatory residential real

estate exposures should be modified in any way to avoid unintended impacts on the ability of

otherwise credit-worthy borrowers who make a smaller down payment to purchase a home.”

Endgame proposal p. 71.

66

With respect to potential competitive effects, the agencies add that “[w]ithout the adjustment

relative to Basel III risk weights in this proposal, marginal funding costs on residential real estate

and retail credit exposures for many large banking organizations could have been substantially

lower than for smaller organizations not subject to the proposal. Though the larger organizations

would have still been subject to higher overall capital requirements, the lower marginal funding

costs could have created a competitive disadvantage for smaller firms.” Endgame proposal pp.

499-500.

67

Basel Committee on Banking Supervision, Calculation of RWA for credit risk, paragraph 22.34,

footnote 3 (effective Jan. 1, 2023).

68

Delta risk would be defined as “the risk of loss that could result from changes in the value of a

position due to small changes in underlying risk factors.”

69

Vega risk would be defined as “the risk of loss that could arise from changes in the value of a

position due to changes in the volatility of the underlying exposure.”

70

Curvature risk would be defined as “the incremental risk of loss of a market risk covered position